Breaking the Substance Barrier: IFSCA Introduces Third-Party Fund Management Model in GIFT IFSC

The International Financial Services Centres Authority (IFSCA) has approved a landmark reform that could redefine the future of cross-border fund management in India.

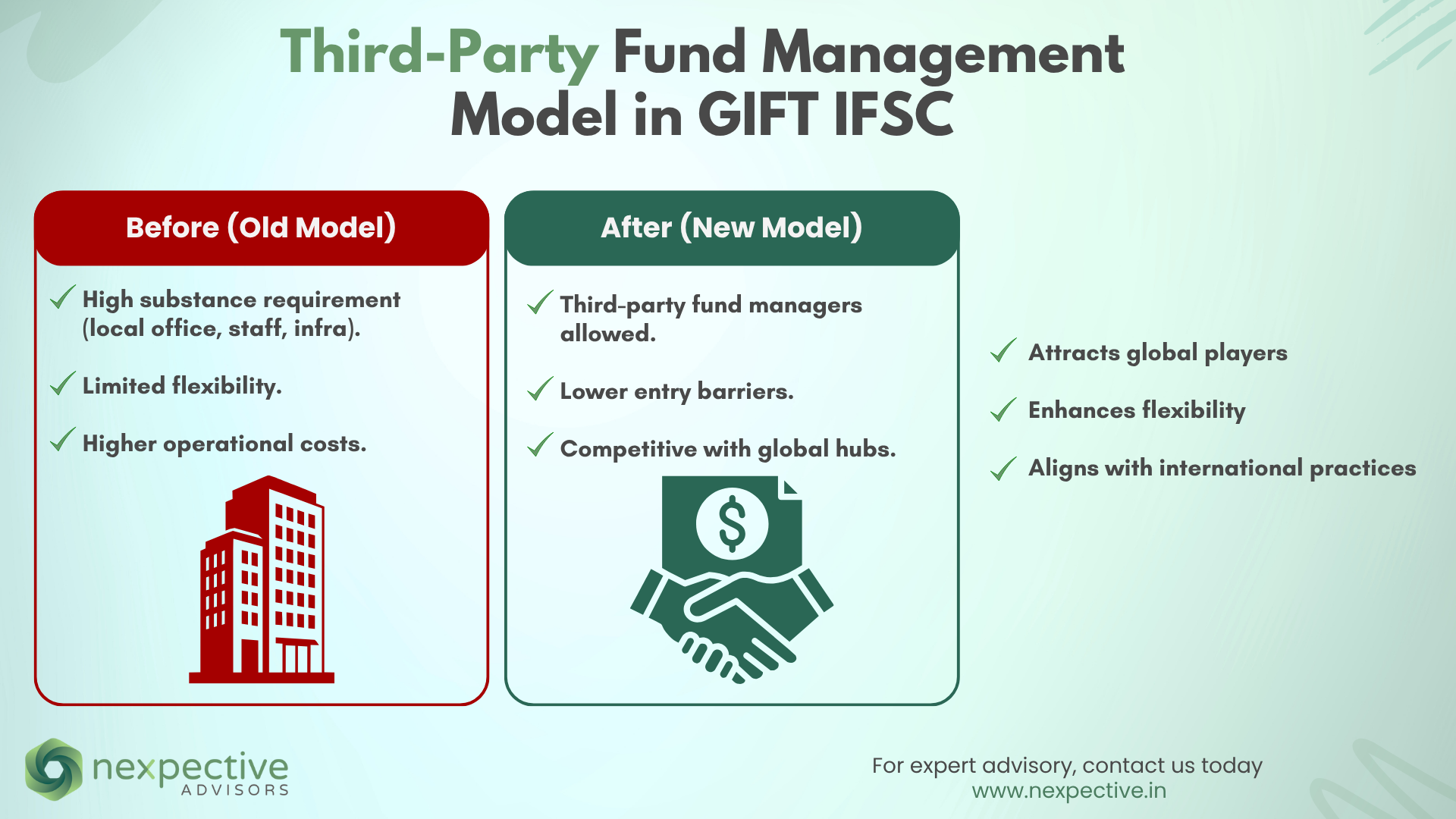

At its 24th meeting held on June 24, 2025, the regulator introduced the Third-Party Fund Management Services (TFMS) framework. This framework allows foreign and domestic managers to operate funds in GIFT IFSC without meeting the substance requirement — i.e., without establishing a physical office, hiring staff, or originating investment proposals from within the IFSC.

Often referred to as the “platform play”, this move is expected to open India’s fund ecosystem to a broader pool of global and domestic managers, aligning GIFT IFSC with international standards while introducing safeguards unique to India.

Understanding the Substance Requirement

Under the IFSCA (Fund Management) Regulations, 2025, any Fund Management Entity (FME) wishing to launch funds in GIFT IFSC had to:

- Incorporate a legal entity in GIFT IFSC.

- Employ qualified local professionals.

- Ensure investment proposals originated from its GIFT IFSC office.

These requirements ensured regulatory oversight, governance, and accountability. However, they also created high entry barriers, discouraging:

- Foreign GPs looking to test Indian investor appetite.

- Emerging managers or family offices lacking resources for a full-fledged setup.

The TFMS framework addresses this bottleneck directly.

The TFMS Model – A Platform-Based Approach

How It Works

- External Fund Manager (Domestic or Foreign):

- Focuses on investment strategy and investor engagement.

- No requirement to set up a local entity or meet substance norms.

- Registered FME (Host Platform):

- Already licensed with IFSCA.

- Assumes full regulatory responsibility, including compliance, governance, risk management, reporting, and investor grievance redressal.

- Fund Structure:

- Applicable only to Restricted Schemes (non-retail funds).

- Corpus capped at USD 50 million per fund.

- Each fund must appoint a dedicated Principal Officer for governance.

Essentially, the External Fund Manager “plugs into” the infrastructure of a Registered FME, avoiding the cost and complexity of independent establishment.

Global Benchmarking – TFMS in Other Jurisdictions

The TFMS model is common in Singapore, Mauritius, and Luxembourg:

- Singapore:

- Uses Variable Capital Companies (VCCs) and umbrella funds.

- Licensed FMCs handle compliance while external managers focus on portfolios.

- By 2025, over 1,900 VCCs with USD 260B+ AUM were registered.

- Mauritius:

- Licensed platforms allow external managers to launch funds quickly.

- Hosts USD 80B+ in cross-border flows annually; ~900 funds domiciled.

- Attracts emerging managers through cost efficiency and tax treaty benefits.

- Luxembourg:

- World’s second-largest fund hub with EUR 5.6T AUM.

- UCITS/AIFMD framework allows delegation of portfolio management.

- Strong investor protection via CSSF supervision.

India’s TFMS safeguards:

- USD 500,000 additional net worth requirement for FMEs offering TFMS.

- USD 50M corpus cap per scheme.

Why This Matters – Industry Impact

The TFMS framework could reshape India’s fund ecosystem:

- For Foreign GPs:

- Offers a low-cost, low-commitment entry to test India.

- Ideal for “toe-in-the-water” market pilots.

- For Emerging Managers and Family Offices:

- Enables quick launches without high compliance overhead.

- Provides institutional-grade oversight via host FMEs.

- For Registered FMEs:

- Creates new revenue streams by hosting third-party funds.

- Positions FMEs as strategic gateways for global capital.

By effectively saying: “You don’t have to move in, you just need a reliable host”, GIFT IFSC has signalled its intent to be an investment gateway.

Challenges and Considerations Ahead

While promising, the TFMS Model faces some hurdles:

- Fund Size Cap – USD 50M:

- Too small for institutional strategies; global hubs impose no such caps.

- Additional Net Worth Requirement:

- USD 500K could restrict smaller FMEs from becoming platforms.

- “Skin in the Game” Ambiguity:

- Unclear if FMEs must invest in TFMS funds, despite lacking control over portfolios.

- Regulatory & Reputational Risk:

- FMEs bear full liability while external managers drive performance.

- Standalone Platforms Prohibited:

- FMEs must launch at least one of their own funds in addition to hosting external ones.

The Road Ahead – What Needs to Change

For TFMS to succeed in India, IFSCA must address these pain points:

- Revisit Fund Size Cap: Increase to USD 200M+ or replace with stronger disclosure and governance norms.

- Clarify Capital & Investment Rules: Specify whether net worth requirement is platform-wide or per fund; define “skin in the game” for TFMS funds.

- Allow Standalone Platforms: Encourage specialised hosting businesses similar to Luxembourg’s delegation model.

- Set Eligibility Criteria for External Managers: Restrict to fit-and-proper, credible managers with proven track records.

- Promote Commercial Flexibility: Allow FMEs and external managers to freely negotiate fees, carried interest, branding, and delegation terms.

Conclusion – A Strategic Evolution

The Third-Party Fund Management Model is one of the most significant reforms for India’s financial ecosystem in recent years. By lowering entry barriers, it creates a credible platform for:

- Foreign GPs to test India.

- Emerging managers to scale quickly.

- Registered FMEs to expand offerings.

While the framework balances global competitiveness, practical entry, and regulatory prudence, its ultimate success depends on how IFSCA fine-tunes key provisions.

Done right, TFMS can transform GIFT IFSC into a global capital gateway, rivaling Singapore, Mauritius, and Luxembourg in fund-hosting capability.

This is Part 1 of a two-part series on TFMS in GIFT IFSC.

Read Part 2: Global Perspectives on TFMS – Lessons for GIFT IFSC

(Comparative analysis of Singapore, Mauritius, and Luxembourg models).