Mandatory Policies for New IFSC Entities in GIFT City: IFSCA Compliance Framework to Start Operations

Establishing a business in GIFT City’s International Financial Services Centre (IFSC) offers access to a globally competitive regulatory and tax environment. However, registration with the International Financial Services Centres Authority (IFSCA) is only the first step. Before commencing operations, every regulated entity must implement a structured compliance and governance framework. At the core of this framework are the mandatory policies for IFSC entities, which form the operational foundation for regulatory compliance, risk management, and investor protection.

These policies are not merely documentation formalities. They demonstrate an entity’s readiness to operate in a regulated international financial ecosystem. Whether the entity is a Broker Dealer, Investment Adviser, Fund Management Entity, or TechFin service provider, implementing these policies is essential to meet IFSC compliance requirements in GIFT City and ensure sustainable and compliant operations.

Mandatory Policies Required Under IFSCA for Starting Operations

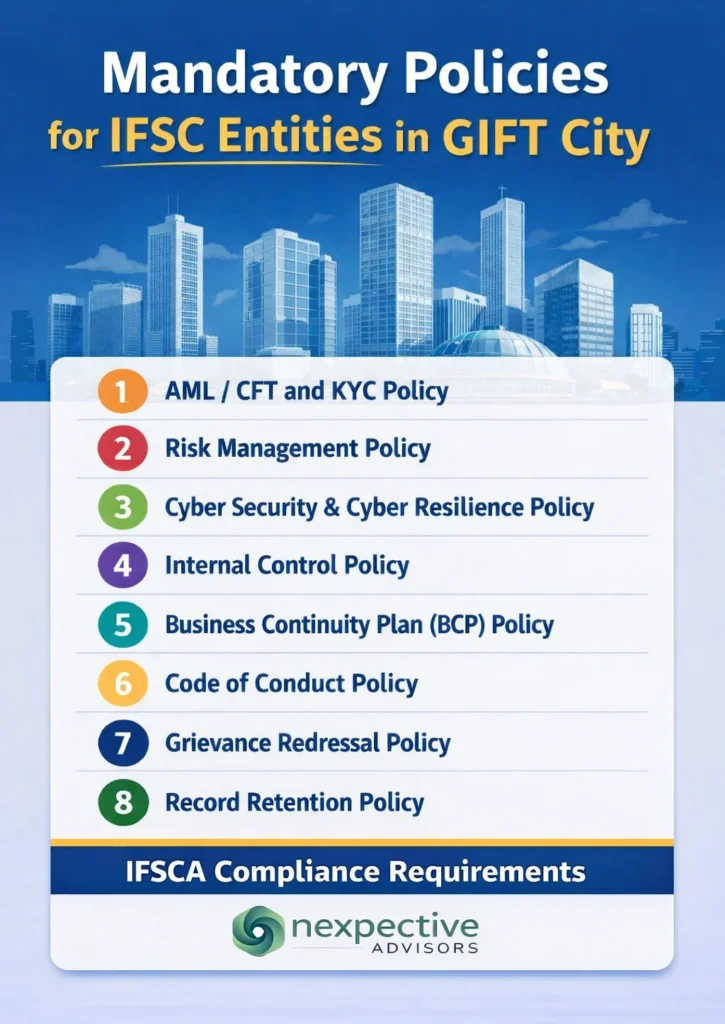

IFSCA regulations require regulated entities to establish internal systems, controls, and governance mechanisms before starting business. As part of the IFSCA mandatory policy framework, new IFSC entities must implement the following eight core policies:

- AML / CFT and KYC Policy

- Risk Management Policy

- Cyber Security and Cyber Resilience Policy

- Internal Control Policy

- Business Continuity Plan (BCP) Policy

- Code of Conduct Policy

- Grievance Redressal Policy

- Record Retention Policy

These policies collectively form the backbone of the IFSCA compliance policies for intermediaries and other regulated entities. They ensure that the organisation operates with appropriate safeguards, protects client interests, and maintains operational resilience. Regulators expect these policies to be properly drafted, approved, implemented, and operational before the entity commences its regulated activities.

For new applicants and registered entities, understanding these policy requirements for IFSC registration is essential to avoid regulatory gaps and ensure smooth commencement of operations.

Understanding the Role and Importance of Each Mandatory Policy

AML / CFT and KYC Policy

The AML KYC policy in IFSC is the most critical compliance requirement. IFSC entities operate in a global financial environment where clients, transactions, and investments may involve multiple jurisdictions. This policy establishes procedures for client onboarding, identity verification, risk classification, and ongoing transaction monitoring.

Its primary objective is to prevent money laundering, terrorist financing, and financial crime. It also ensures compliance with international regulatory standards and protects the entity from regulatory penalties and reputational risk. A well-implemented AML policy strengthens regulatory trust and is essential for maintaining the integrity of financial operations.

This becomes particularly critical for entities planning Fund Management Entity registration in GIFT IFSC, where AML supervision and investor protection standards are closely monitored.

Cyber Security and Cyber Resilience Policy

In today’s digital financial ecosystem, cyber risk is one of the most significant operational risks. The cyber security policy required by IFSCA ensures protection of IT infrastructure, financial systems, and client data.

This policy defines access controls, system security measures, data protection protocols, and incident response mechanisms. It helps prevent cyber attacks, data breaches, and system disruptions. Given that most IFSC entities rely heavily on technology platforms, cyber security compliance is not only a regulatory requirement but also a critical business necessity.

This is equally relevant for organisations establishing Global Capability Centres in GIFT IFSC, where data security, operational resilience, and technology governance are central regulatory expectations.

Risk Management Policy

The risk management policy establishes a structured approach to identifying, assessing, and managing risks associated with business operations. IFSC entities face various types of risks, including operational risk, regulatory risk, financial risk, and technology risk.

This policy ensures that risk exposure is continuously monitored and controlled. It helps management make informed decisions, maintain financial stability, and operate within acceptable risk parameters. Effective risk management is essential for long-term sustainability and regulatory compliance.

Internal Control Policy

The internal control policy focuses on ensuring operational integrity and protecting client assets. It defines approval processes, authority levels, and segregation of duties within the organisation.

This policy helps prevent fraud, errors, and unauthorised activities. It also ensures accurate financial reporting and compliance with regulatory requirements. Strong internal controls demonstrate good governance and increase regulatory confidence in the entity’s operations.

Business Continuity Plan (BCP) Policy

The business continuity plan ensures that the entity can continue operations during unexpected disruptions such as system failures, cyber incidents, natural disasters, or infrastructure outages.

This policy includes disaster recovery procedures, data backup mechanisms, and alternate operational arrangements. It helps minimise operational downtime and ensures continuity of services. For regulated IFSC entities, maintaining uninterrupted operations is essential to protect clients and maintain market confidence.

Grievance Redressal Policy

Investor protection is a key regulatory objective in IFSC. The grievance redressal policy establishes a structured mechanism for handling client complaints and resolving disputes.

This policy ensures that complaints are properly recorded, investigated, and resolved within defined timelines. It promotes transparency and strengthens investor confidence. A well-implemented grievance framework reflects the organisation’s commitment to fair and responsible conduct.

Record Retention Policy

The record retention policy ensures that financial, client, and regulatory records are properly maintained and preserved. IFSC regulations require entities to retain records for specified periods to support compliance, audit, and regulatory inspection.

Proper record maintenance ensures transparency, accountability, and regulatory readiness. It also helps in responding to regulatory queries, compliance audits, and internal reviews.

Code of Conduct Policy

The code of conduct policy establishes ethical standards and professional behaviour expected from employees and management. It promotes integrity, transparency, and responsible business conduct.

This policy helps manage conflicts of interest, ensures fair treatment of clients, and strengthens organisational governance. Ethical conduct is a fundamental expectation in the IFSC regulatory environment.

When These Policies Must Be Implemented

A common misconception is that policies can be developed after starting operations. In reality, IFSCA expects entities to implement these policies before commencing regulated activities.

| Stage | Requirement |

|---|---|

| Registration stage | Policies should be drafted and approved |

| Before starting operations | Policies must be fully implemented |

| Ongoing operations | Policies must be followed, reviewed, and updated |

Implementing policies at the initial stage ensures compliance readiness and avoids regulatory risks. These policies form an essential part of the IFSCA compliance checklist for new entities.

Support in Drafting and Implementing Mandatory IFSC Policies

Drafting IFSC-compliant policies requires a clear understanding of regulatory expectations and practical business operations. Generic or template-based policies often fail to meet regulatory standards or operational needs.

Professional support helps ensure that policies are properly structured, aligned with IFSCA regulations, and customised to the entity’s specific business model. This includes drafting policies, defining procedures, implementing governance frameworks, and ensuring readiness for regulatory inspections and compliance audits.

Properly designed policies not only meet regulatory requirements but also strengthen operational efficiency and governance.

Conclusion

The mandatory policies for IFSC entities are the foundation of regulatory compliance and operational readiness. They ensure that the organisation operates responsibly, manages risk effectively, and protects client interests.

Implementing these policies before starting operations is essential to meet IFSC compliance requirements in GIFT City and operate successfully within the regulated financial ecosystem. These policies support governance, ensure regulatory alignment, and build long-term credibility.

As IFSC continues to grow as a global financial hub, a strong policy framework will remain essential for every new entity entering this ecosystem.

FAQs: Mandatory Policies for IFSC Entities

-

Are mandatory policies required before starting IFSC operations?

Yes. IFSC entities must implement mandatory policies before commencing regulated business activities.

-

Which is the most important policy for IFSC entities?

The AML / CFT and KYC policy is considered the most critical due to its role in preventing financial crime and ensuring regulatory compliance.

-

Who is responsible for implementing IFSC compliance policies?

The Board of Directors, Principal Officer, and Compliance Officer are responsible for implementing and monitoring compliance policies.

-

Can IFSC entities use standard policy templates?

Generic templates may not meet regulatory expectations. Policies should be customised based on the entity’s business model and regulatory requirements.

-

What happens if mandatory policies are not implemented?

Failure to implement policies may lead to regulatory action, penalties, operational restrictions, or licence cancellation.